You may lose the main residence exemption if you sell after 1 July 2019

What happened?

Currently, any individual (regardless of their tax residency status) who sells their home can qualify for either:

- the full main residence exemption (e.g. if the residence has been used as a main residence throughout the whole ownership period – whether through actual use or imputed use1); or

- the partial main residence exemption (e.g. if the residence has been used partly as main residence and partly for income-producing purposes during the ownership period).

However, there is currently a Bill2 before Parliament that, if enacted, will mean that any individual vendor that is a non-resident (for tax purposes) at the time they sign a contract to sell their home will no longer be able to qualify for the full or partial main residence exemption – regardless of how long the home has actually been used as a main residence.

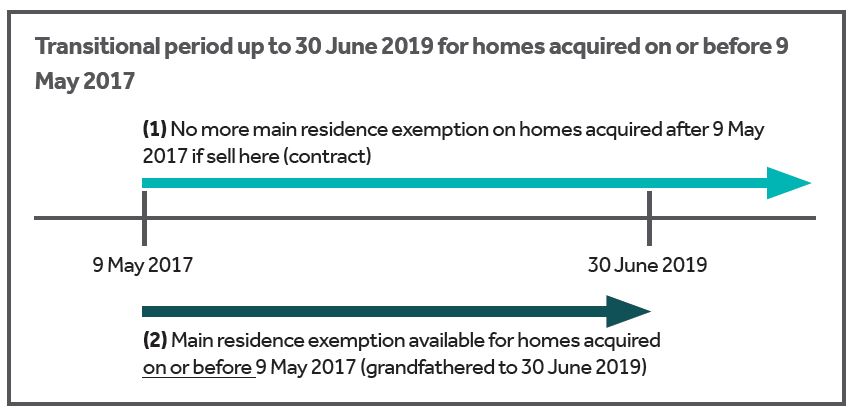

The time from when this proposed measure will apply depends on the time when the home was acquired – see opposite.

When will these proposed changes apply from?

The timeline below illustrates that the full or partial main residence exemption will not be available for non-residents signing a contract of sale to sell their homes:

- after 9 May 2017 – for homes acquired after 9 May 2017; and

- after 30 June 2019 – for homes acquired on or before 9 May 2017.

These measures can therefore have a profound effect on individuals who have used their post CGT home as a main residence for a substantial period of time (and saw the value of the property also increase substantially) and then eventually sell the residence (i.e. sign the contract for sale) when they are non-residents for tax purposes.

For example, take an individual who bought property in 1986 (i.e. post CGT and before 9 May 2017) and have been using the property as his/her main residence throughout this time. In July 2018 the individual leaves Australia permanently and establishes a permanent place of abode overseas (other facts and circumstances also indicate that the individual has become a non-resident for tax purposes).

If the non-resident individual were now to sell his/her residence and the date the sale contract is signed is:

- on or before 30 June 2019 – no tax would be payable because the non-resident individual seller would still qualify for the main residence exemption;

- after 30 June 2019 – tax would be payable3 because the non-resident individual seller would not qualify for the main residence exemption.

There are also flow on effects for estate planning purposes (e.g. whether a beneficiary of a deceased estate that sells a property that was the deceased’s main residence would qualify for the main residence exemption when the beneficiary sells the house, would depend on the residency status of both the deceased and the beneficiary).

What other issues arise from these proposed changes?

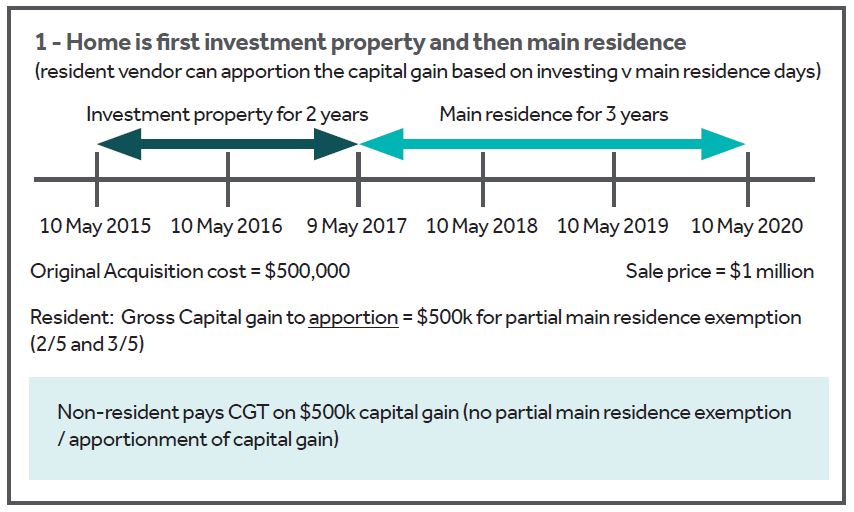

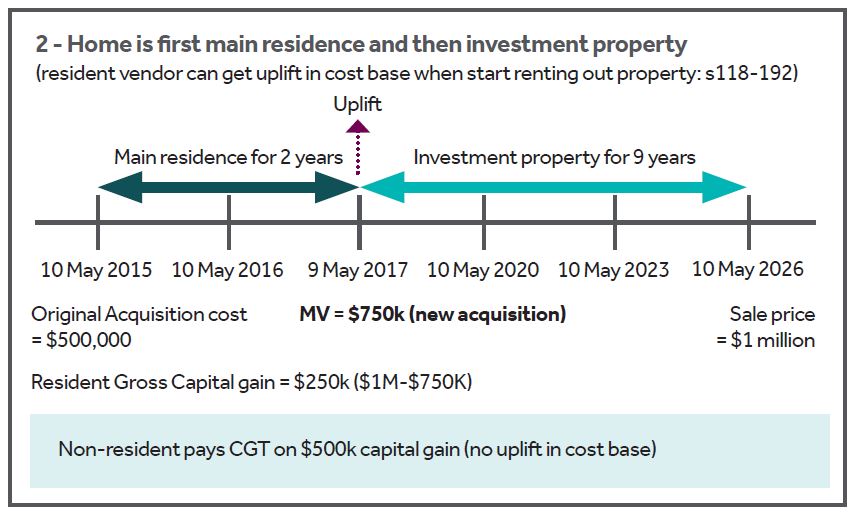

Individuals who are non- residents at the time of signing the sale contract to sell their property that have been used as both a main residence and an investment property will lose their ability to:

- apportion the main residence exemption (for a home that was first used as an investment property and then used as a main residence); or

- get a step-up in cost base (for a home that was first used as a main residence and then used as an investment property.

The 2 diagrams that follow visually display these phenomena.

Further thoughts

At the time of writing, these proposed changes are not yet law. However, once (and if) these proposed changes do become law, it will be very important for vendors to determine their tax residency status before they sign a contract to sell a property that would potentially qualify for the full or partial main residence exemption.

Important to note, there will be no apportionment of the time the individual used the home as a main residence – the only test is residency status at the time of signing the contract of sale.

This “all or nothing approach” can lead to catastrophic consequences for individuals that have used their properties as main residences for an extended period of time but sell their properties (i.e. sign the contract to sell the properties) when they are non-residents for tax purposes.