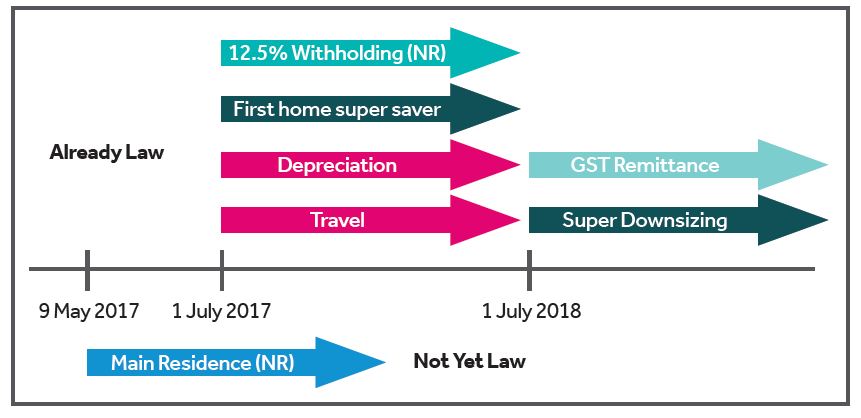

Because property ownership is such an important issue for many people, we want to remind everyone of some recent changes to:

- The tax treatment associated with residential rental properties (e.g. travel deduction and depreciation changes);

- Withholding tax obligations on purchasers of property:

- 12.5% CGT withholding on the sale of any property for $750,000 or more unless the vendor has a tax clearance certificate evidencing the vendor’s Australian tax residency;

- 10% GST withholding on the sale of new residential premises (from 1 July 2018);

- Superannuation measures impacting home ownership (e.g. first home super saver scheme and superannuation downsize incentive); and

- Stamp duty and land tax issues (different in each state – not discussed here).

There is also a proposal to abolish the main residence exemption for taxpayers who are no longer Australian tax residents. Furthermore, foreign investors need permission from the Foreign Investment Review Board (“FIRB”) before purchasing residential properties (excluding some new dwellings) or agricultural land in Australia.

The main tax measures and date of application of the measures are set out in the timeline below.

A brief outline of the main tax issues affecting property transactions follows below.

1. Changes affecting residential rental properties in 2018

From 1 July 2017, individuals, discretionary trusts and self-managed superfunds will no longer be able to claim travel expenses (e.g. motor vehicle expenses, taxi or car hire costs, airfares or public transport costs or meals or accommodation related to the aforementioned travel) incurred to inspect residential rental properties. These deductions will also not be included in the cost base or reduced cost base of the rental property.

However, taxpayers may still claim travel expenses to inspect commercial premises and residential premises used to carry on a business (e.g. premises used as a retirement village). Property management expenses paid to real estate agents (which may involve real estate agents incurring travel expenses to inspect the residential rental property) will still be deductible.

Also, from 1 July 2017 the depreciation on plant and equipment (e.g. washing machines and refrigerators) in residential rental units will be severely limited depending on whether:

- the plant and equipment was acquired before or after 9 May 2017;

- the plant and equipment have been previously used;

- the plant and equipment have been used in the taxpayer’s residence before; or

- whether the plant and equipment is installed in new residential premises.

2. Changes to the foreign resident CGT withholding rule in 2018

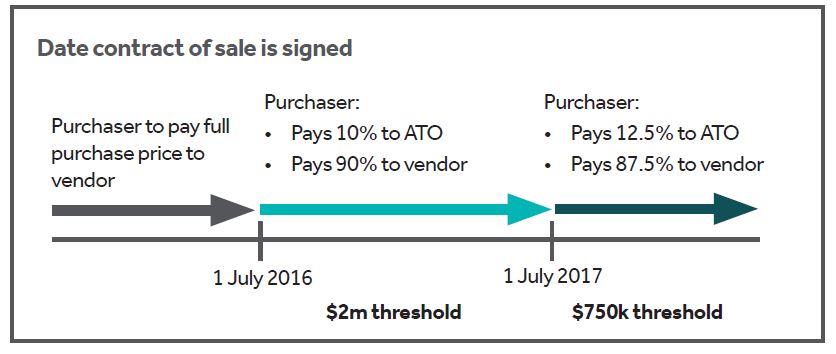

From 1 July 2017, a 12.5% non-final withholding tax applies when a non-resident sells property in Australia for more than $750,000 (note, in 2017 the CGT withholding rate was 10% and the sale price benchmark was $2 million). Therefore, from 1 July 2017, a non-resident vendor will only be paid 87.5% of the sale price because 12.5% must be withheld by the purchaser and paid to the ATO as a prepayment of tax on behalf of the foreign vendor.

This measure will result in extra compliance measures (e.g. tax resident vendors will also be subject to these rules unless they obtain Australian Taxation Office (“ATO”) tax clearance certificates) but carve outs from this rule are available (e.g. for purchases of Australian real property valued at less than $750,000 from 1 July 2017).

We can help tax resident vendors to obtain ATO tax clearance certificates to avoid application of the 12.5% withholding rule when they are selling a residential property for $750,000 or more. A tax clearance certificate – basically an ATO certificate confirming that the vendor is an Australian tax resident – provided to the purchaser before settlement date would enable such a vendor to receive 100% of the purchase price from the purchaser instead of only 87.5% of the purchase price at settlement.

If more than one vendor is involved, each vendor must apply separately for a tax clearance certificate and if any of the vendors fails to provide such a tax clearance certificate to the purchaser, the purchaser must withhold 12.5% of the purchase price (in proportion to each vendor’s interest in the property).

3. New GST withholding rule on the sale of new residential premises from 1 July 2018

For the 2018 income tax year, purchasers of new residential premises pay a GST inclusive amount to the seller (i.e. GST is included in the purchase price so the purchaser pays GST to the seller and the seller must remit the GST to the ATO).

However, from 1 July 2018, purchasers of new residential premises will have to pay the GST component of the purchase price directly to the ATO:

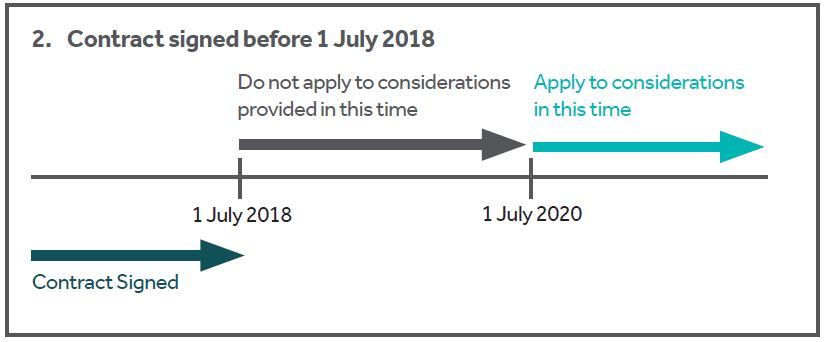

- For sale contracts signed on or after 1 July 2018, the purchaser will be required to withhold and pay 10% of GST to the ATO on the day the consideration is provided (i.e. at instalment dates or at settlement if lump sum at settlement); and

- For sale contracts signed before 1 July 2018, the 10% GST withholding rule will only apply to payments made on or after 1 July 2020 (i.e. there is a 2-year transitional period where GST withholding will not apply to consideration provided in this transitional period).

This new GST withholding regime does not apply to the sale of used residential properties or the sale of new or used commercial premises.

4. Superannuation measures impacting home ownership

4.1 First Home Super Saver Scheme

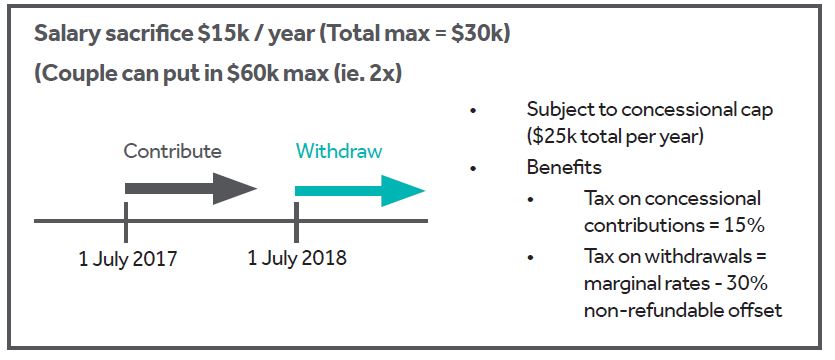

From 1 July 2017, a first home buyer can salary sacrifice a maximum of $15,000 a year (take care not to breach the $25,000 concessional contributions cap) to save for a deposit to buy a first home. The maximum amount that can be saved in such a way is $30,000. Provided the buyer’s partner does not already own his or her first home, the couple can put in a maximum of $60,000 ($30,000 x 2) to buy a first home.

Money saved in this way can only be withdrawn from the superannuation fund from 1 July 2018 with strict rules applying on how to use such withdrawn money (e.g. must buy a home within a certain time and the ATO must be notified of the withdrawal).

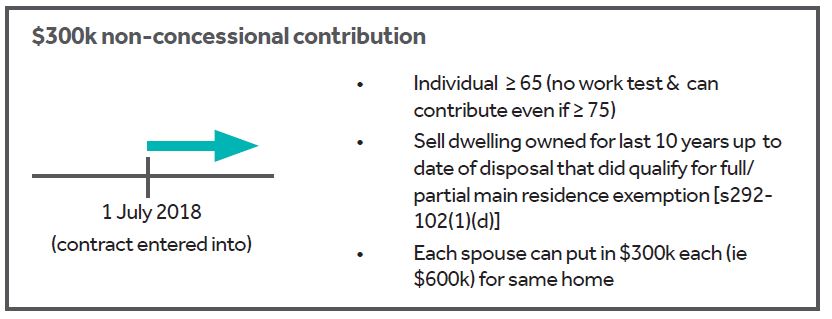

4.2 Super downsizer incentive available from 1 July 2018

From 1 July 2018, an individual aged 65 or above, may make a $300,000 non-concessional contribution (and coupled with a spouse the total contribution can be $600,000) from the proceeds of selling his or her home (i.e. provided the home was owned for the last 10 years up to the date of disposal and would have qualified for either a full or partial main residence CGT exemption).

Individuals need not buy a replacement residence or to satisfy the so-called “work-test” (i.e. work for at least 40 hours over 30 consecutive days) to be able to contribute to their superannuation fund. Furthermore, this incentive can only be utilised once by each person.

The biggest drawcard of this incentive is that non-concessional contributions made pursuant to this incentive will not be subject to the $1.6 million total superannuation cap. Therefore, individuals that already have more than $1.6 million in superannuation can use this super downsizer incentive to potentially contribute an additional $600,000 to superannuation.

5. Proposal that foreign residents will no longer qualify for the main residence exemption

Currently, any individual (regardless of their tax residency status) who sells their home can qualify for either:

- the full main residence exemption (e.g. if the residence has been used as a main residence throughout the whole ownership period – whether through actual use or imputed use); or

- the partial main residence exemption (e.g. if the residence has been used partly as main residence and partly for income-producing purposes during the ownership period).

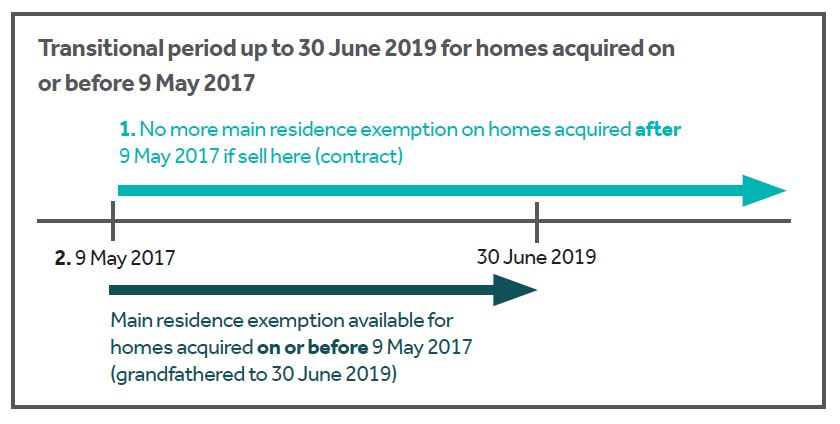

However, a Bill before Parliament, if enacted, will mean that any individual vendor that is a non-resident (for tax purposes) at the time they sign a contract to sell their home will no longer be able to qualify for the full or partial main residence exemption – regardless of how long the home has actually been used as a main residence.

The timeline below illustrates that the full or partial main residence exemption will not be available for non-residents signing a contract of sale to sell their homes:

- after 9 May 2017 – for homes acquired after 9 May 2017; and

- after 30 June 2019 – for homes acquired on or before 9 May 2017.

Assuming the Bill becomes law in its current format, a non-resident who disposes of his/her main residence in the 2018 income tax year, will not qualify for the main residence exemption if the dwelling was purchased after 9 May 2017.